The U.S. Securities and Exchange Commission has issued its clearest interpretation yet of how crypto assets are treated under federal securities laws, marking a decisive break from years of regulatory overreach. Chairman Paul Atkins announced the framework at the Digital Chamber summit, while the SEC said the move will give markets long-overdue clarity.

In a statement posted on X, Atkins said:

“After more than a decade of uncertainty, this interpretation will provide market participants with a clear understanding of how the Commission treats crypto assets under federal securities laws.”

He went further in a separate post, writing:

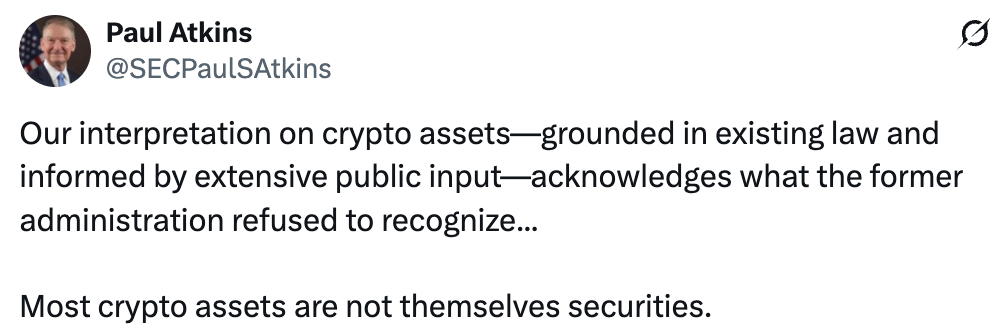

“Our interpretation on crypto assets—grounded in existing law and informed by extensive public input—acknowledges what the former administration refused to recognize…

Most crypto assets are not themselves securities.”

At the center of the shift is a formal token taxonomy. The SEC now separates digital assets into categories like commodities, collectibles, tools, and payment stablecoins, none of which are treated as securities. Only tokenized versions of traditional financial instruments, labeled “digital securities,” fall under SEC jurisdiction. As Atkins explained in his remarks:

“Our interpretation… establishes four asset categories that are not deemed to be securities… digital commodities, digital collectibles, digital tools, and payment stablecoins… Only one crypto asset class remains subject to securities laws… digital securities.”

A Direct Reversal Of The Gensler Era

Under prior SEC leadership, the regulatory trajectory was clear: expand the definition of securities to pull as much of the crypto industry as possible under the agency’s control. That included attempts to classify developers, platforms, and even software interfaces as broker-dealers. If successful, it would have forced anyone building or operating crypto infrastructure to register with the SEC and implement strict KYC (Know Your Customer) and AML (Anti-Money Laundering) programs.

In practice, that meant:

- Open-source developers could face regulatory obligations

- Wallet providers and interfaces could be treated like financial institutions

- Everyday users interacting with protocols could be pushed into identity-linked systems

The implications were massive, not just for innovation, but for privacy.

The Line Has Now Been Drawn

The new SEC interpretation shuts that door. By clearly separating the asset itself from the investment contract around it, the Commission is narrowing its own jurisdiction. Most crypto assets, especially Bitcoin, are now explicitly outside securities law unless they are part of a capital-raising scheme. That distinction matters.

Securities law is one of the primary legal pathways regulators use to impose financial surveillance requirements. Broker-dealers are required by law to collect user data, monitor transactions, and report activity to authorities. Expanding that framework to crypto would have effectively turned open networks into permissioned systems. This interpretation blocks that outcome.

A Major Win For Privacy

This is the part many are missing: this is a privacy decision as much as a regulatory one. By declining to classify most crypto activity as securities-related, the SEC is also stepping back from the ability to mandate KYC/AML controls at the protocol level.

That means:

- No blanket requirement for identity verification tied to Bitcoin usage under SEC authority

- No forced registration of developers building non-custodial tools

- No automatic extension of Wall Street surveillance rules into decentralized networks

In short, it preserves a key property of Bitcoin: permissionless access.

Bitcoin’s Position Just Got Stronger

The framework also reinforces what markets have already assumed: Bitcoin sits firmly in commodity territory, not securities.

Working alongside the Commodity Futures Trading Commission, the interpretation aligns regulatory treatment with Bitcoin’s design: no issuer, no central control, no promise of profit from a third party.

That clarity reduces one of the biggest lingering risks around Bitcoin in the U.S.: regulatory misclassification.

Why This Matters

This decision determines whether the future of money looks like Bitcoin or like a bank.

If regulators had succeeded in classifying crypto infrastructure as securities activity, using Bitcoin could have required identity checks, monitoring, and permission from intermediaries.

Instead, this interpretation keeps the door open for peer-to-peer, permissionless money, where users can transact without needing approval or surveillance baked into the system.

That’s not just a win for Bitcoin. It’s a win for financial autonomy.