The U.S. Treasury has delivered a new report to Congress examining how emerging technologies can be used to combat illicit finance in the digital asset ecosystem. The document, titled “Report to Congress From the Secretary of the Treasury on Innovative Technologies to Counter Illicit Finance Involving Digital Assets,” analyzes how regulators and law enforcement agencies are tracking criminal activity on blockchains while assessing how the broader crypto industry is evolving.

The report was prepared as part of ongoing federal efforts to evaluate risks and tools related to digital assets, including blockchain analytics, artificial intelligence, and other monitoring technologies used to detect suspicious activity across public ledgers. But buried within the report is a notable acknowledgment about financial privacy on blockchains, one that has drawn attention across the Bitcoin and crypto industry.

Treasury explicitly states that using Bitcoin and crypto privacy mixers is not inherently unlawful.

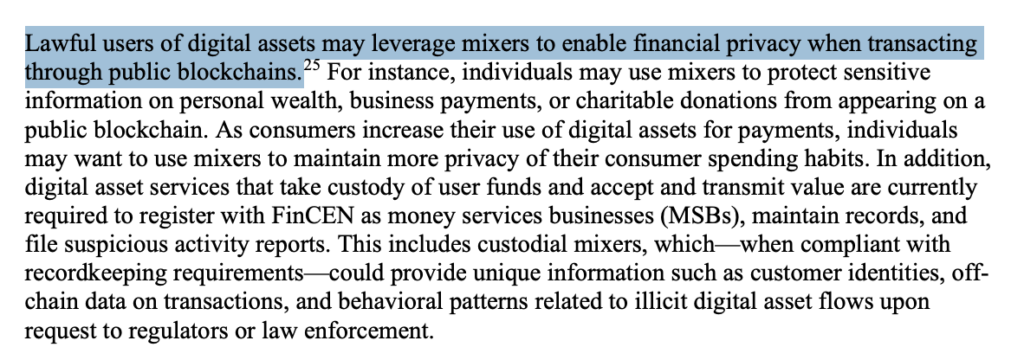

In the report, officials write: “Lawful users of digital assets may leverage mixers to enable financial privacy when transacting through public blockchains.”

The document explains that because most blockchain networks are fully transparent, individuals may use privacy tools to prevent sensitive financial information, such as personal wealth, business payments, or charitable donations, from becoming permanently visible on a public ledger.

Privacy mixers, sometimes referred to as tumblers, work by pooling together digital asset transactions from multiple users and redistributing them in a way that obscures the original source of funds. These tools have long been controversial because they can be used both by ordinary users seeking privacy and by criminals attempting to conceal illicit proceeds.

The Treasury report acknowledges this dual-use reality. It notes that mixers have been used by ransomware groups, darknet markets, and state-sponsored hackers to obscure stolen funds. At the same time, the document makes clear that privacy itself is a legitimate reason for using these technologies, particularly in systems where transaction histories are permanently visible.

The report also highlights the rapid growth of blockchain activity worldwide. According to Treasury’s analysis, the number of transactions occurring across digital asset networks has expanded dramatically in recent years, reaching billions of transactions per month globally. As adoption grows, regulators are increasingly relying on blockchain analytics tools to monitor patterns of activity and identify potential illicit finance networks.

While the report focuses primarily on enforcement capabilities and technological tools available to regulators, its acknowledgment of lawful privacy use cases marks a notable shift in tone compared to earlier enforcement-driven narratives surrounding mixers and other privacy technologies.

For advocates of open financial systems, the language represents an important distinction: not every attempt to protect financial activity on a transparent blockchain should be treated as suspicious or criminal.

As Bitcoin and other digital assets continue to mature, the tension between transparency, surveillance, and financial privacy is likely to remain a central debate. The Treasury’s report suggests regulators are increasingly recognizing that privacy tools can serve legitimate purposes in a financial system built on public ledgers.

For supporters of financial sovereignty and digital privacy, the statement in the report is significant. It amounts to a rare official acknowledgment from the U.S. government that using privacy tools on public blockchains can be lawful, a major win for the principle of financial privacy in the digital age.